── Attaching core tidyverse packages ──────────────────────── tidyverse 2.0.0 ──

✔dplyr 1.1.4 ✔readr 2.1.5

✔forcats 1.0.0 ✔stringr 1.5.1

✔ggplot2 3.5.2.9002✔tibble 3.3.0

✔lubridate 1.9.4 ✔tidyr 1.3.1

✔purrr 1.1.0

── Conflicts ────────────────────────────────────────── tidyverse_conflicts() ──

✖dplyr::filter() masks stats::filter()

✖dplyr::lag() masks stats::lag()

ℹ Use the conflicted package (<http://conflicted.r-lib.org/>) to force all conflicts to become errors

Attaching package: ‘data.table’

The following objects are masked from ‘package:lubridate’:

hour, isoweek, mday, minute, month, quarter, second, wday, week,

yday, year

The following objects are masked from ‘package:dplyr’:

between, first, last

The following object is masked from ‘package:purrr’:

transpose

Attaching package: ‘kableExtra’

The following object is masked from ‘package:dplyr’:

group_rows

Setup complete (packages loaded: tidyverse, data.table, ggsci, moments, knitr, kableExtra).

3 Independence vs. Zero Correlation

Independence means no influence between events, while correlation measures linear relationship strength.

Independence implies zero correlation, but zero correlation does not imply independence.

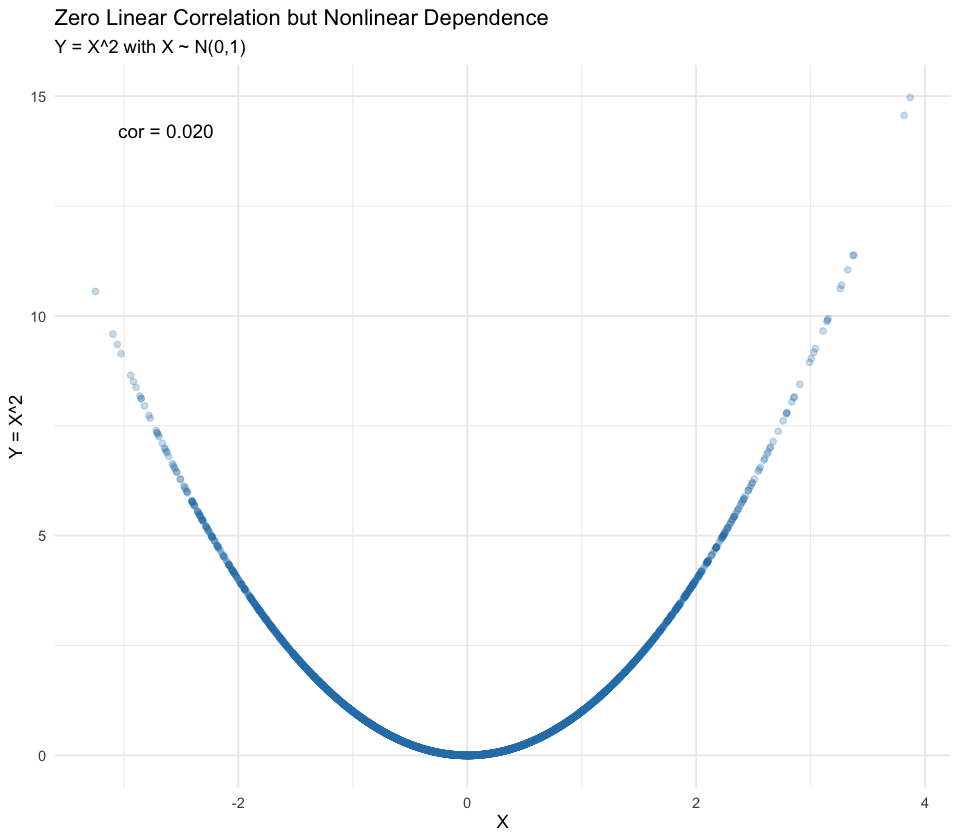

E.g., \(X\) and \(Y = X^2\) have zero correlation but are not independent.

# ---- Zero Correlation but NOT Independence: Y = X^2 ----# Idea: X ~ N(0,1); define Y = X^2. Then cor(X,Y) ~ 0 (symmetry cancels linear relation),# yet Y is a deterministic function of X so they are NOT independent.set.seed(2025)n <-5000X <-rnorm(n)Y <- X^2r_xy <-cor(X, Y)cat(sprintf("Sample correlation cor(X, Y=X^2) = %.4f (near 0)\n", r_xy))

We got \(\rho_{X,Y}=0.0198\). It seems to be close to zero, but we need a statistical test to confirm this formally.

→ Test for significance of the correlation coefficient

cor.test(X, Y)

Pearson's product-moment correlation

data: X and Y

t = 1.4027, df = 4998, p-value = 0.1608

alternative hypothesis: true correlation is not equal to 0

95 percent confidence interval:

-0.007887062 0.047529726

sample estimates:

cor

0.01983657

💡 Q: Based on the output of cor.test, what is the p-value for the correlation test? What can you conclude about the correlation between the two variables? Are \(X\) and \(Y\) independent? Write your answer in the cell below.

A: [Type your answer here]

Distinguish the two expressions:

correlation coefficient equals zero ❌

correlation coefficient (statistically) indifferent from zero ✅

Now let’s visualize \(Y=X^2\) by plotting the scatter plot.

library(ggplot2)options(repr.plot.width =8, repr.plot.height =7)scatter_df <-data.frame(X = X, Y = Y)p1 <-ggplot(scatter_df, aes(X, Y)) +geom_point(alpha =0.25, color ='#2c7fb8') +annotate('text', x =min(X)+0.2, y =max(Y)*0.95,label =paste0('cor = ', sprintf('%.3f', r_xy)),hjust =0, size =4) +labs(title ='Zero Linear Correlation but Nonlinear Dependence',subtitle ='Y = X^2 with X ~ N(0,1)',x ='X', y ='Y = X^2') +theme_minimal()print(p1)

The following figure shows the scatter plot of two assets with various correlation coefficients.

4 Descriptive Statistics on Asset Returns

# ---- Load Asset Returns Data ----asset_df <-read_csv("https://raw.githubusercontent.com/my1396/FIN5005-Fall2025/refs/heads/main/data/asset_returns.csv")print("Preview: first 6 rows of asset returns data frame:")head(asset_df) %>%round(2)

[1] "Preview: first 6 rows of asset returns data frame:"

A tibble: 6 × 3

Asset_A

Asset_B

Asset_C

<dbl>

<dbl>

<dbl>

17.89

4.31

9.94

10.30

4.17

10.55

20.87

14.16

6.61

18.21

22.33

9.58

17.49

2.23

10.23

29.87

15.72

8.97

We define a summary statistics function to compute the statistics of interest.

quick_summary <-function(x) {# Function to compute basic descriptive statisticsdata.frame(n =length(x),mean =mean(x),sd =sd(x),var =var(x),skewness = moments::skewness(x),kurtosis = moments::kurtosis(x),row.names =NULL )}

The summary statistic table is generated as follows:

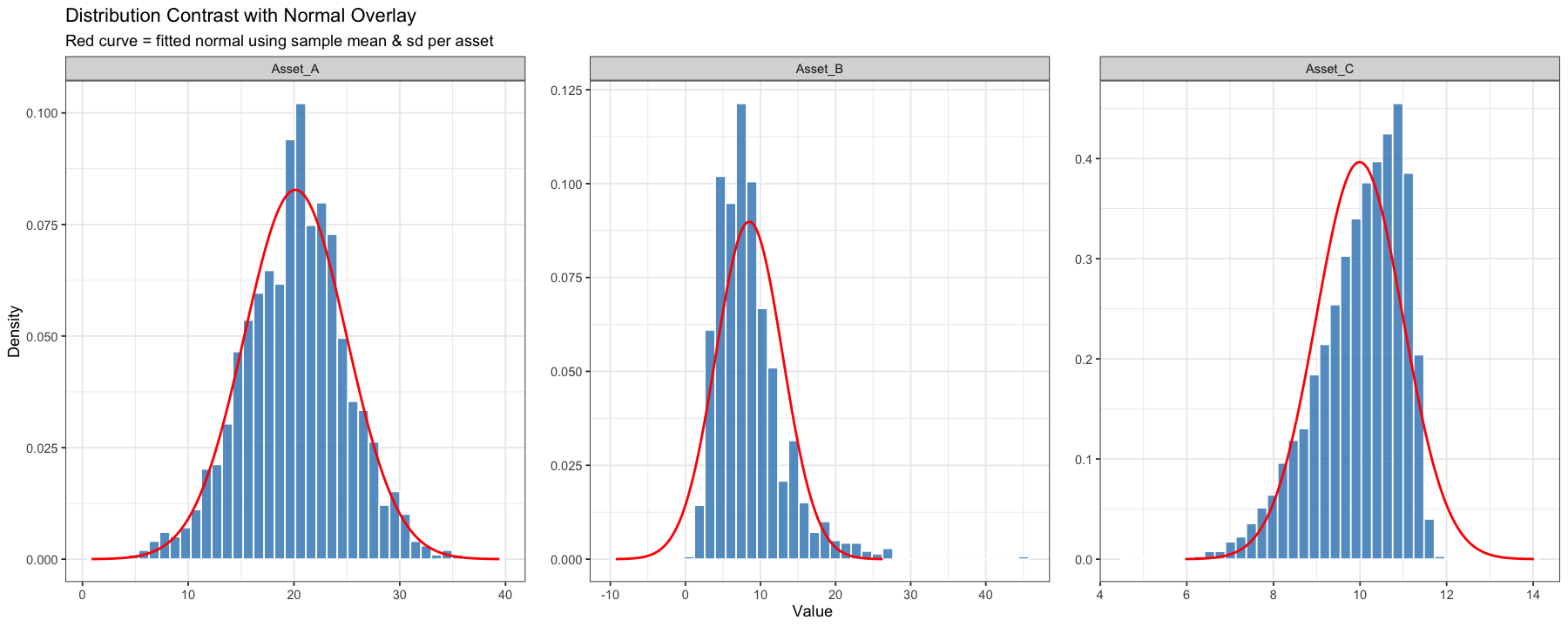

Plot the histograms of the asset returns to visualize their distributions.

# ---- Visualization: Histograms with Normal Density Overlay ----# Convert to long formcombined <- asset_df %>%pivot_longer(cols =everything(), names_to ="type", values_to ="value")# Compute per-type mean & sd and create normal curve pointsnorm_params <- combined %>%group_by(type) %>%summarise(mu =mean(value), sigma =sd(value), .groups ='drop')norm_curve <- norm_params %>%group_by(type) %>%do({ mu <- .$mu; sigma <- .$sigma x <-seq(mu -4*sigma, mu +4*sigma, length.out =400)tibble(value = x, density =dnorm(x, mu, sigma))})options(repr.plot.width =15, repr.plot.height =6)ggplot(combined, aes(value)) +geom_histogram(aes(y =after_stat(density)), bins =40, fill ="#3182bd", alpha =0.8, color ="white") +geom_line(data = norm_curve, aes(value, density), color ="red", linewidth =0.8) +facet_wrap(~ type, scales ="free", nrow =1) +labs(title ="Distribution Contrast with Normal Overlay",subtitle ="Red curve = fitted normal using sample mean & sd per asset",x ="Value", y ="Density") +theme(panel.spacing.x =unit(1.2, "lines"))

💡 Q: Answer the following questions based on the summary statistics and the distribution plots:

Which asset has the highest mean return?

Which asset is the most risky? and which one has the most stable returns?

Which asset shows the positive skewness and what does it mean?

If an investor prefers assets with low risk and return distributions with tails close to normal, which asset is most appropriate?

Based on mean and standard deviation, which asset has the best risk–return trade-off (highest mean per unit of risk)?

A: [Type your answer here]

5 Large Sample Gives More Accurate Estimates

We have a variable \(X\sim N(0,5^2).\)

Normal distribution notation: \(X\sim N(\mu, \sigma^2)\) means that \(X\) is normally distributed with mean \(\mu\) and variance \(\sigma^2.\)

The second parameter is the variance, NOT the standard deviation.

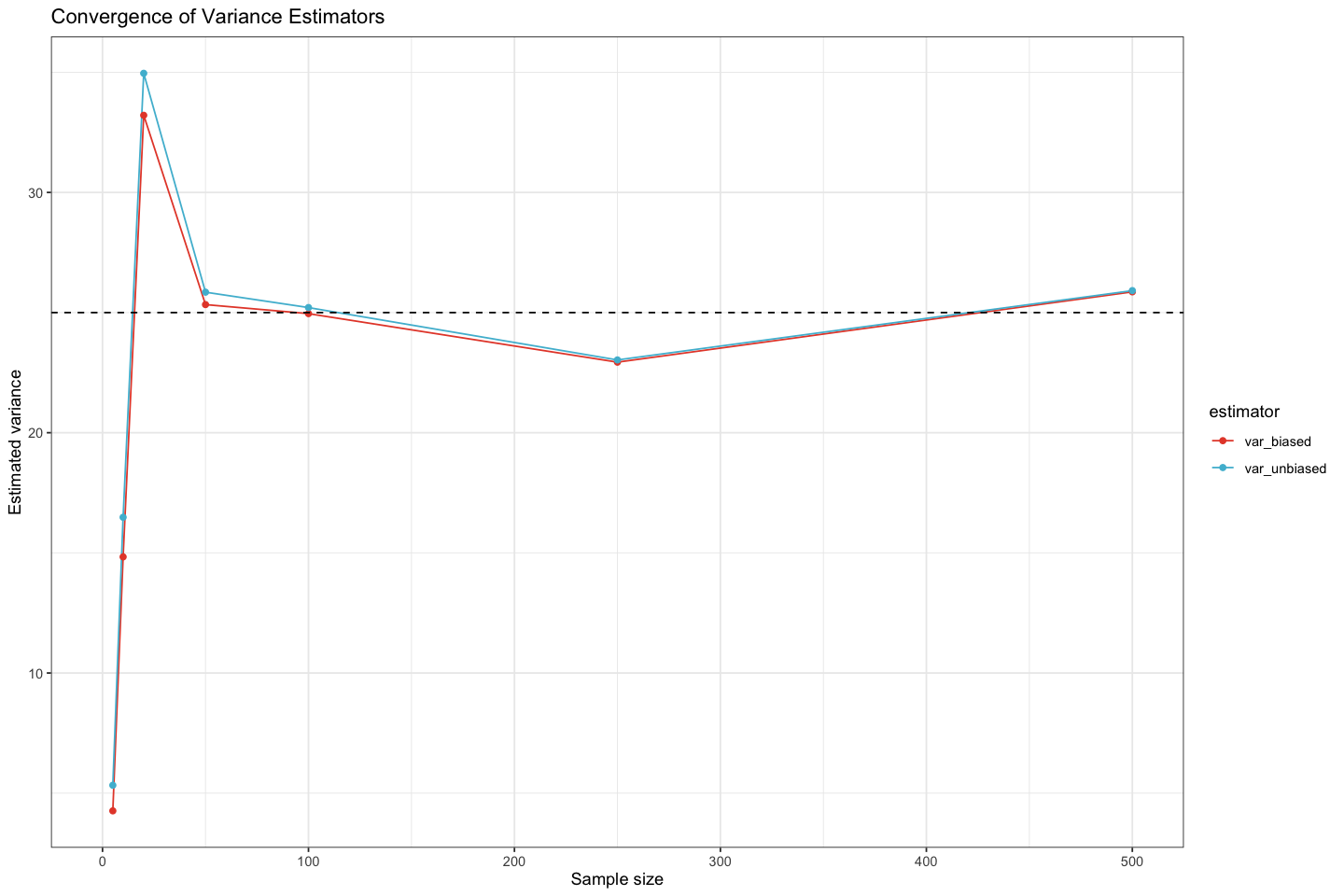

Now we draw random samples of size 5, 10, 10, … until 5000 from this distribution and compute the sample mean and standard deviation for each sample.

For each sample, we compute the biased and unbiased sample variance

The biased sample variance is computed as \[\frac{1}{n}\sum_{i=1}^n (x_i - \bar{x})^2.\]

The unbiased sample variance is computed as \[\frac{1}{n-1}\sum_{i=1}^n (x_i - \bar{x})^2\]

# ---- Simulation: Sample vs Population variance ----set.seed(2025) # for reproducibilitytrue_var <-25# sd^2 with sd=5, true population variancesample_sizes <-c(5, 10, 20, 50, 100, 250, 500, 1000, 5000) # varying sample sizes from 5 to 500results <-lapply(sample_sizes, function(n){ x <-rnorm(n, mean =0, sd =5)data.frame("sample_size"= n, "var_biased"=mean((x -mean(x))^2), "var_unbiased"=var(x))}) %>% dplyr::bind_rows()cat('Variance estimators: var_n (biased, divide by n) vs var_n1 (unbiased, divide by n-1).\n')results

Variance estimators: var_n (biased, divide by n) vs var_n1 (unbiased, divide by n-1).

A data.frame: 9 × 3

sample_size

var_biased

var_unbiased

<dbl>

<dbl>

<dbl>

5

4.262707

5.328384

10

14.832929

16.481032

20

33.210505

34.958426

50

25.332410

25.849398

100

24.957059

25.209150

250

22.936725

23.028840

500

25.862610

25.914439

1000

25.574182

25.599782

5000

25.301658

25.306719

💡 Q: Based on the variance estimates for different sample sizes:

As the sample size increases, how do the sample variance estimates compare to the true variance \(25\)?

Does the sample variance converge to the true variance as the sample size increases?

What is the difference between the biased and unbiased sample variance estimators?

A: [Type your answer here]

# ---- Plot: Convergence of variance estimators ----results_long <- results %>% tidyr::pivot_longer(var_biased:var_unbiased, names_to ="estimator", values_to ="value") %>% dplyr::mutate(estimator = dplyr::recode(estimator, var_n ="Divide by n", var_n1 ="Divide by n-1"))options(repr.plot.width =12, repr.plot.height =8)ggplot(results_long, aes(sample_size, value, color = estimator)) +geom_line() +geom_point() +scale_color_npg() +geom_hline(yintercept = true_var, linetype ="dashed") +xlim(c(0,500)) +labs(title ="Convergence of Variance Estimators", y ="Estimated variance", x ="Sample size")

Warning message:

“Removed 4 rows containing missing values or values outside the scale range

(`geom_line()`).”

Warning message:

“Removed 4 rows containing missing values or values outside the scale range

(`geom_point()`).”

6 Correlated Asset Returns

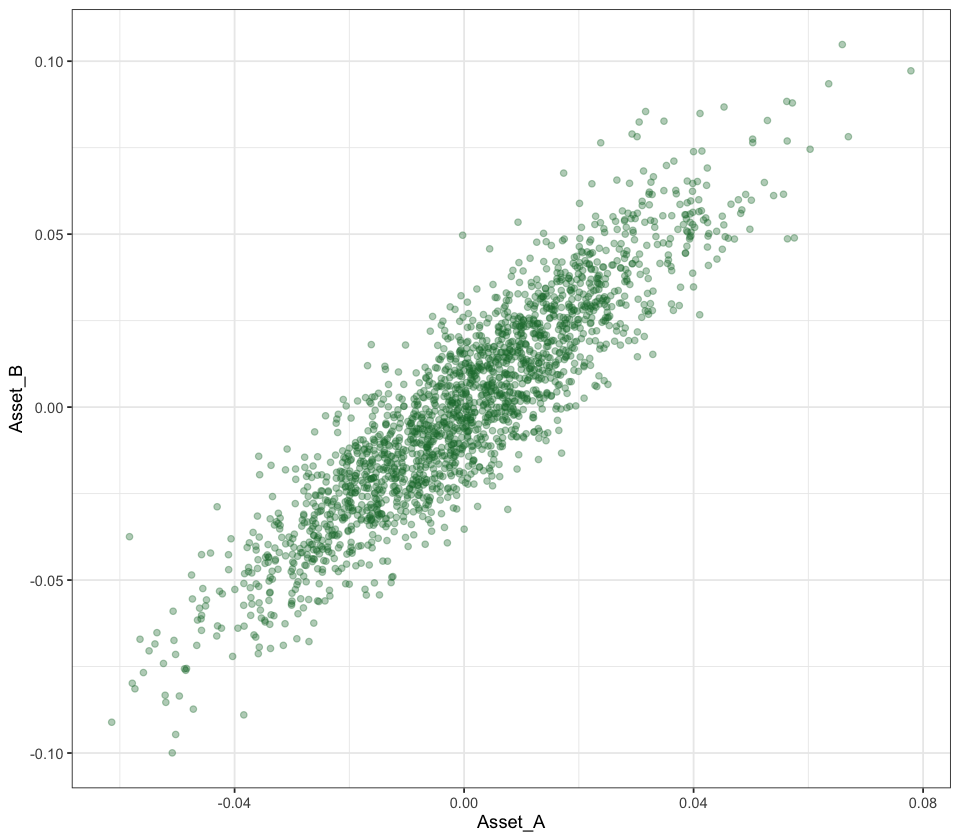

We will simulate repeated samples of two (correlated) asset return series and compare the sampling distributions of their sample means and the distribution of the portfolio mean (equal weights).

# ---- Load Correlated Asset Returns Data ----X_demo <-read_csv("https://raw.githubusercontent.com/my1396/FIN5005-Fall2025/refs/heads/main/data/correlated_asset_returns.csv")colnames(X_demo) <-c("Asset_A", "Asset_B") # Rename columns for clarityX_demo %>%as.data.table() %>% .[, lapply(.SD, function(x) if (is.numeric(x)) round(x, 4) else x)] %>%print(digits =4)

Plot the scatter plot of the two asset returns to visualize their relationship.

options(repr.plot.width =8, repr.plot.height =7)ggplot(X_demo, aes(Asset_A, Asset_B)) +geom_point(alpha =0.35, color ='#1b7837')

💡Q: What is the correlation between the two asset returns? How do their prices move together?

A: [Type your answer here]

Exercise

Following the steps below, you will compute the mean and standard deviation of the two asset returns, construct a portfolio, and analyze its properties.

Step 1: Calculate the standard deviation of Asset A and B returns, respectively.

Step 2: Construct a equally weighted portfolio of the two assets. Calculate the portfolio returns. \[

E[r_p] = \frac{1}{2} (E[r_A] + E[r_B])

\]

Step 3: Calculate the standard deviation of the portfolio returns, \(\text{sd}(r_p)\).

Step 4: Calculate the average of the volatility of Asset A and B (using results in Step 1). Compare it with the volatility of the portfolio returns.

6.1 Reflection

How does correlation between assets influence the portfolio mean’s variability? Write 3–4 sentences interpreting for a diversified vs concentrated investment decision.