\(I_t\) is the inflation rate; \(\Delta I_t = I_t - I_{t-1}\) is the first difference of the inflation rate;

\(u_t\) is the unemployment rate;

\(\varepsilon_t\) is the error term.

We remove the first two quarters due to missing value in the first observation and the change in the rate of inflation.

Regression result for OLS.

lm_phillips <-lm(delta_infl ~ unemp, data = data %>%tail(-2))stargazer(lm_phillips, type ="html", title ="Phillips Curve Regression",notes ="<span>*</span>: p<0.1; <span>**</span>: <strong>p<0.05</strong>; <span>***</span>: p<0.01 <br> Standard errors in parentheses.",notes.append = F)

Phillips Curve Regression

Dependent variable:

delta_infl

unemp

-0.090

(0.126)

Constant

0.492

(0.740)

Observations

202

R2

0.003

Adjusted R2

-0.002

Residual Std. Error

2.822 (df = 200)

F Statistic

0.513 (df = 1; 200)

Note:

*: p<0.1; **: p<0.05; ***: p<0.01 Standard errors in parentheses.

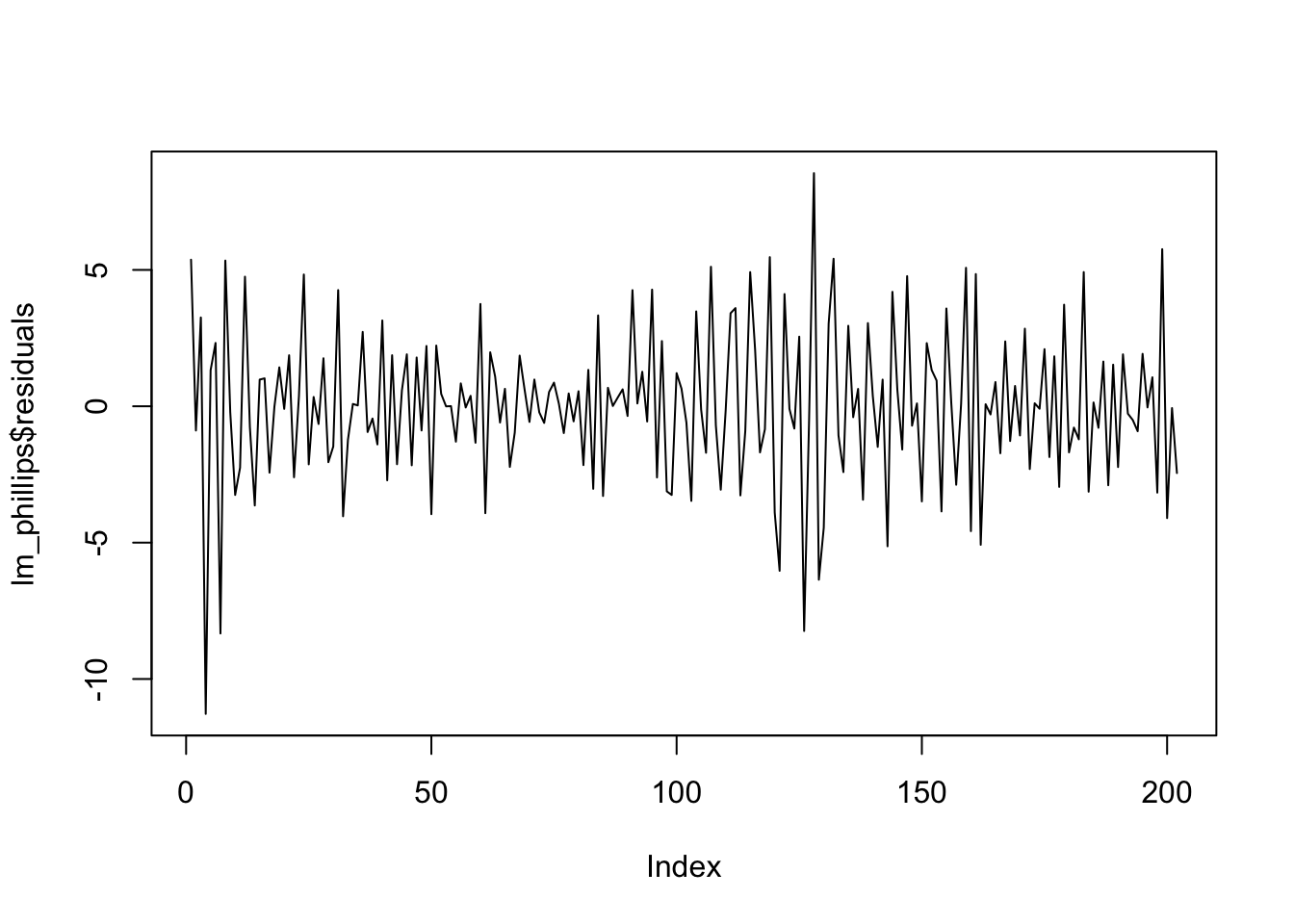

Figure 5.1: Phillips Curve Deviations from Expected Inflation

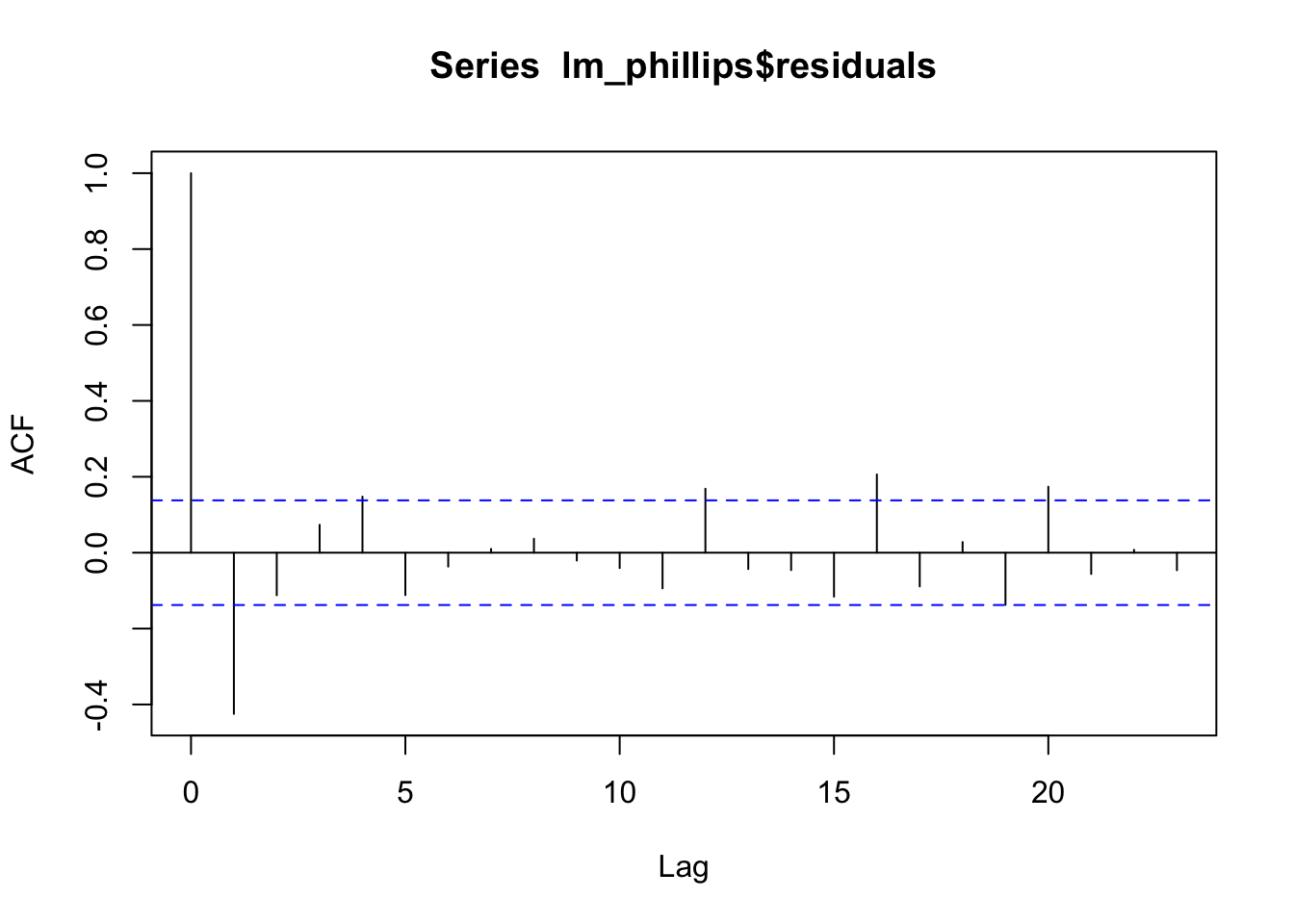

Figure 5.1 shows striking negative autocorrelation. The correlogram tells the same story (Figure 5.2). The blue dotted lines give the values beyond which the autocorrelations are (statistically) significantly different from zero.

acf(lm_phillips$residuals, type='correlation')

Figure 5.2: Correlogram of the residuals

We can get the autocorrelation coefficients by setting plot = FALSE

Now we test the serial correlation of the residuals by regressing \(\varepsilon_t\) on \(\varepsilon_{t-1}\).

\[

\varepsilon_t = \phi\varepsilon_{t-1} + e_t

\]

res <-tibble(res_t = lm_phillips$residuals,res_t1 =lag(lm_phillips$residuals))lm_res <-lm(res_t ~ res_t1, data = res)summary(lm_res)

Call:

lm(formula = res_t ~ res_t1, data = res)

Residuals:

Min 1Q Median 3Q Max

-9.8694 -1.4800 0.0718 1.4990 8.3258

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -0.02155 0.17854 -0.121 0.904

res_t1 -0.42630 0.06355 -6.708 2e-10 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 2.531 on 199 degrees of freedom

(1 observation deleted due to missingness)

Multiple R-squared: 0.1844, Adjusted R-squared: 0.1803

F-statistic: 44.99 on 1 and 199 DF, p-value: 2.002e-10

The regression of the least squares residuals on their past values gives a slope of -0.4263 with a highly significant \(t\) ratio of -6.7078. We thus conclude that the residuals in this models are highly negatively autocorrelated.

5.3 Test for Serial Correlation

Durbin-Watson (DW) test for AR(1)

Breusch-Godfrey test for AR(q)

library(lmtest)dwtest(lm_phillips, alternative ="two.sided") # Durbin Watson test

Durbin-Watson test

data: lm_phillips

DW = 2.8276, p-value = 5.212e-09

alternative hypothesis: true autocorrelation is not 0

bgtest(lm_phillips, order=1) # Breusch-Godfrey test

Breusch-Godfrey test for serial correlation of order up to 1

data: lm_phillips

LM test = 36.601, df = 1, p-value = 1.45e-09

Both tests show strong evidence of AR(1) serial correlation in the errors.

5.4 Consequence for Serial Correlation

The presence of autocorrelation can lead to misleading results as they violate the assumptions of least squares.

The least squares estimator is still a linear unbiased estimator, but is no longer best.

One consequence of the serial correlated errors is that the standard error and \(t\) statistics are not valid anymore. In the case if serial correlation, you can either

Transform the model to remove the serial correlation, or alternatively,

FGLS (Feasible Genralized Least Squares), transform the original equation using, e.g., Cochrane-Orcutt or Prais-Winsten transformation.

This approach assumes strictly exogeneous regressors, that is, NO lagged \(y\) is allowed in the RHS of the equation. See Chapter 12.3 in Wooldridge (2013), Introductory Econometrics: A Modern Approach.

Use serial correlation-robust standard errors

HAC (Heteroskedasticity and autocorrelation consistent) standard errors or Newey-West standard errors.

Infinite Distributed Lag Models

Geomoetric (or Koyck) and Rational Distributed Lag Models.

References

Ex. 12.3, Chap 12 Serial Correlation, Econometric Analysis, Greene 5th Edition, pp 251.